Royalty Pharma – Funding the Next Generation of Medicines

Royalty Pharma, a PM Capital holding, is reshaping how breakthrough medicines are funded and developed.

By Alex Warnaar

In April 2026, Royalty Pharma plc announced that Revolution Medicines Inc (RevMed) received positive results from its highly anticipated Phase 3 trial for daraxonrasib, a potential breakthrough medicine for pancreatic cancer.1

RevMed said its late-stage trial demonstrated daraxonrasib provides patients an ‘unprecedented overall survival benefit’, almost doubling the typical length of survival for pancreatic cancer to 13.2 months, compared to chemotherapy.2

If daraxonrasib secures US Food and Drug Administration (FDA) approval, RevMed could change the standard of care for approximately 70,000 people diagnosed annually with pancreatic cancer in the United States.

Beyond the United States, the medicine could eventually reach other markets and RevMed may run further trials testing daraxonrasib’s applicability in other cancer variants, including lung cancer.3

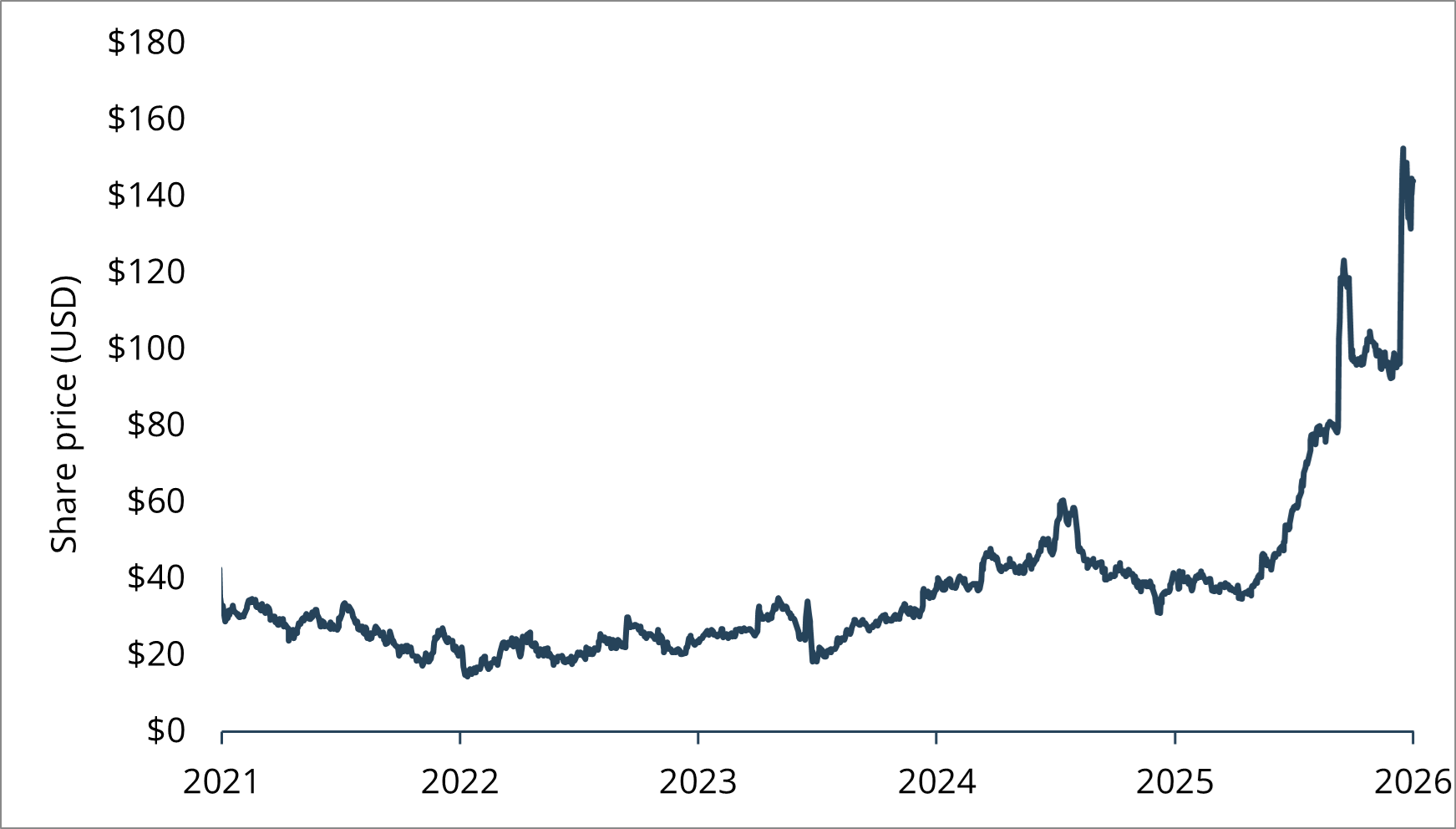

RevMed shares (NASDAQ: RVMD) soared 39% on the daraxonrasib trial news.4

Chart 1: Revolution Medicines share price (US$)

Source: FactSet. Past performance is not indicative of future performance.

Royalty Pharma, the world’s largest lifescience royalties company5, is a key financier of RevMed, having provided up to US$2 billion of funding in June 2025 via a royalty of up to US$1.25 billion on daraxonrasib and a senior secured loan of up to US$750 million.6

The RevMed deal is one of many for Royalty Pharma, which has built its business on finding, and funding, remarkable breakthroughs in science.

Royalty Pharma’s landmark deal occurred in 2014 when it paid US$3.3 billion to acquire royalties on Vertex Pharmaceuticals’ revolutionary, but at the time yet-to-be FDA-approved, cystic fibrosis treatment, owned by an affiliate of the Cystic Fibrosis Foundation7.

Cystic fibrosis (CF) is a rare genetic disease that primarily affects the lungs and digestive system. Over 100,00 patients have been diagnosed globally, often within days of birth. Left untreated, patients with the disease can live relatively short lifespans.8 In 2014, the Cystic Fibrosis Foundation described Royalty Pharma’s funding as a ‘transformational moment for … the entire CF community.’9

A decade on and the deal has also proved transformational for Royalty Pharma. It received US$917 million royalties from its CF franchise in 2025, up 7% on a year earlier, constituting just over a quarter of Royalty Pharma’s total portfolio receipts in 2025.10

Business model & history

A pharmaceutical royalty is a financial arrangement in which an investor receives payments linked to a medicine’s future revenues – but without owning the underlying intellectual property, and without manufacturing or marketing the medicine. The payments are defined contractually and may include milestones related to clinical trial results or FDA approval.

Pharmaceutical royalties arise when new science is discovered by universities, research hospitals, institutes and emerging biotech firms, but the science is commercialised by a pharmaceutical firm with global reach. The pharmaceutical firm in-licenses or acquires the science and often pays the original developer a royalty stream. In some instances, these deals occur bilaterally between two pharmaceutical giants.

Pharmaceutical royalties have existed for decades but it was Pablo Legorreta, a Mexican-American investment banker, who pioneered pharmaceutical royalties as an investment class when he founded Royalty Pharma in 1996 in New York.

Legorreta recognised that universities, research hospitals, institutes and emerging biotech firms often owned valuable medicine royalty rights but preferred upfront cash to invest in other endeavours, rather than waiting for long-term sales.

Indeed, proceeds from deals with Royalty Pharma in 2004 and 2005 allowed the Memorial Sloan Kettering Cancer Center to reinvest and build one of the largest cancer research centers in New York.11

Two decades later, Leggoreta has also recognised that, rather than partnering with a pharmaceutical giant, biotech firms may wish to commercialise the science themselves, and that royalty deals can act as a suitable funding source. The RevMed deal is exactly such a deal.

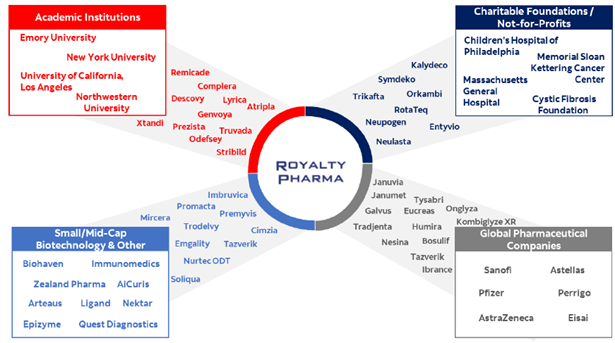

Chart 2: Royalty Pharma deals

Source: Royalty Pharma

Growth prospects

Royalty Pharma is the largest company of its kind in the pharmaceutical industry and listed publicly in 2020. We believe Royalty Pharma has become the partner-of-choice for many life science companies seeking royalty funding - and even the world’s largest pharmaceutical companies.

In March 2026, Royalty Pharma announced a US$500 million deal with Johnson & Johnson to advance the development of JNJ-4804, an investigational medicine for autoimmune diseases.12 The deal is significant because it shows giant pharmaceutical companies are starting to use royalty funding in their capital structure to fund medicine development.

Such is Royalty Pharma’s reputation that securing funding from Royalty Pharma can be a valuable form of endorsement for emerging biotech companies, given its due diligence when funding new medicines and record in backing winners.

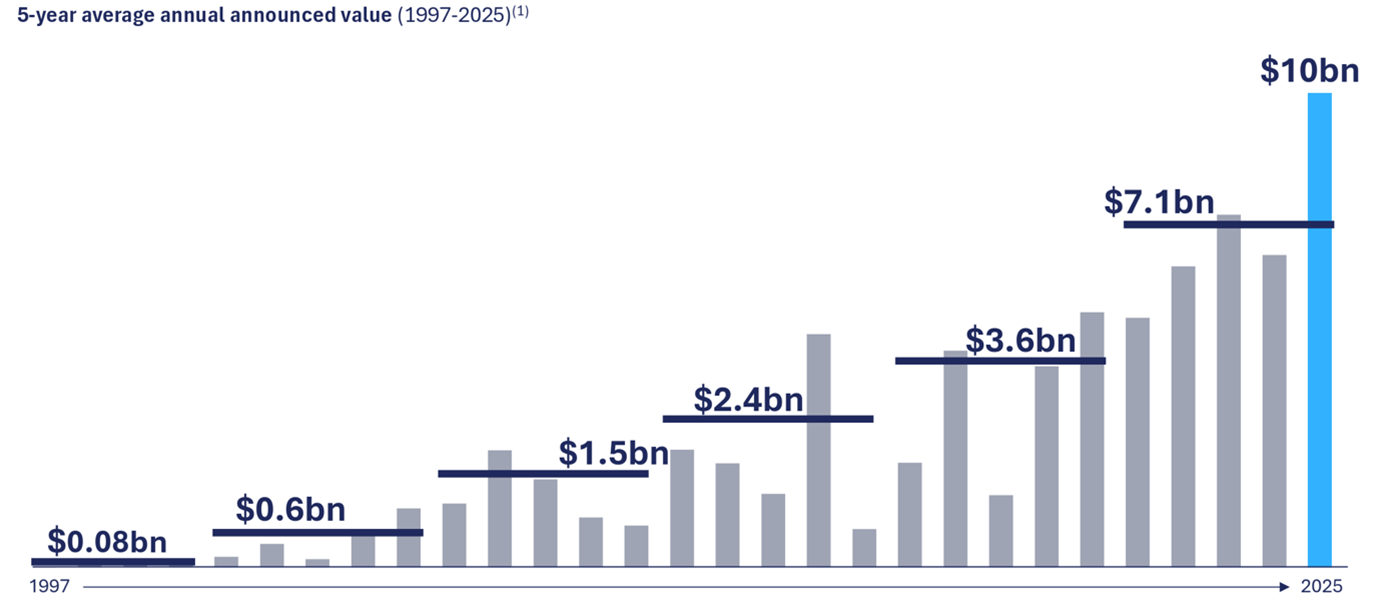

According to Royalty Pharma, the value of all announced royalty transactions has averaged US$6.2 billion per year over the past five years. That figure is more than double that of the previous five years and triple that of 15 years ago.13

Chart 3: Growth in royalty funding over 5-year period (US$)

Source: Royalty Pharma, Corporate Presentation, February 2026, p.12.

Royalty Pharma estimates that 400 lifescience companies need funding annually and that the total addressable market for biotech funding (debt, equity and royalty funding) will exceed US$1 trillion over the next decade.14

Unlike equity funding, royalty financing is non-dilutive and does not involve issuing shares. Unlike traditional debt, royalty funding does not require paying interest or principal repayments. Royalty payments are contingent on product revenues and only made if a medicine generates sales. In most cases, the financier has limited or no involvement in clinical development or pricing decisions.

Conclusion

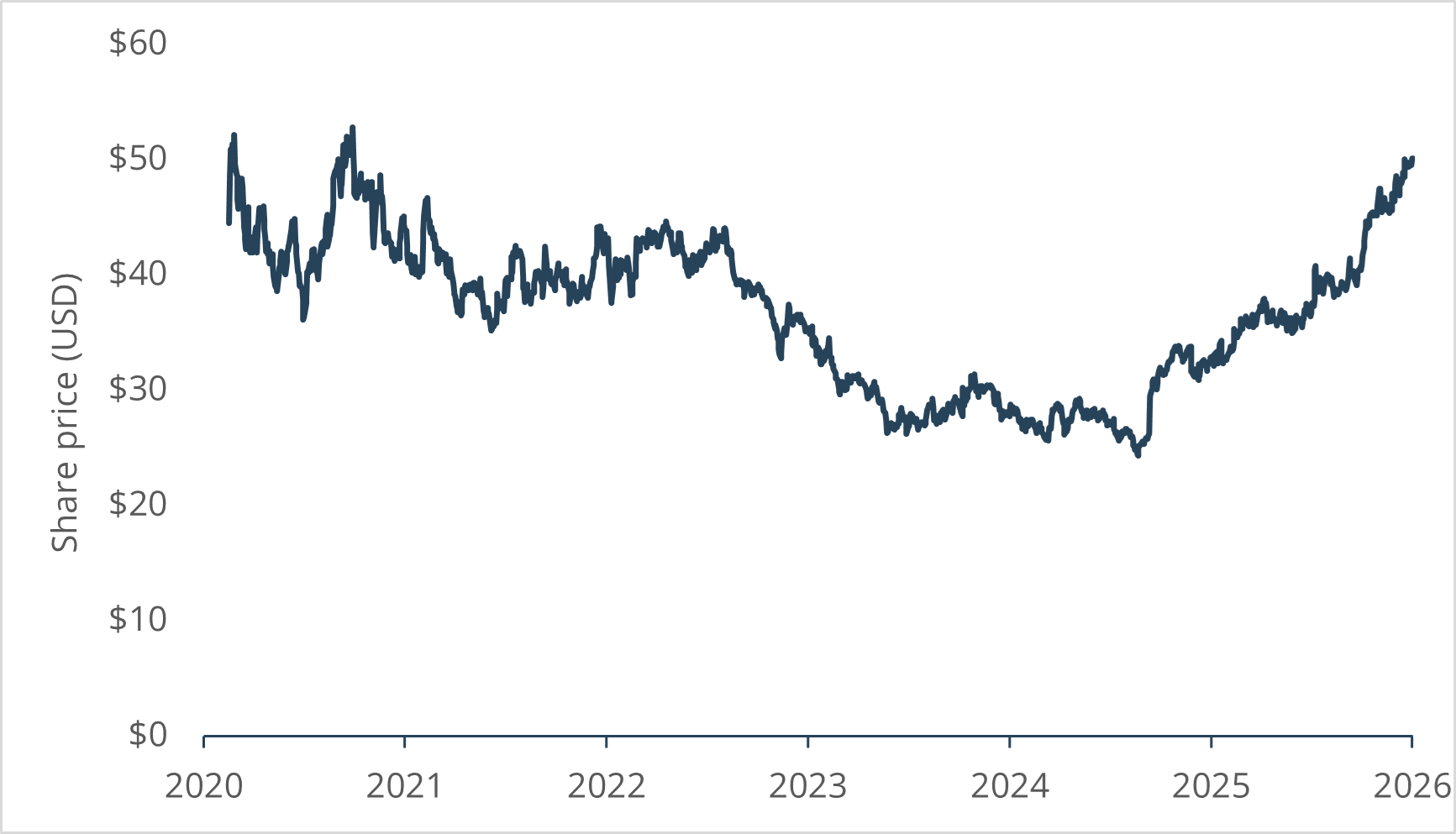

In early 2024, PM Capital initiated a position in Royalty Pharma after sustained share-price weakness. At an unreasonably discounted valuation of under seven times its net royalty receipts, the market at the time attributed little value to Royalty Pharma’s growth prospects or strength of its business model. Royalty Pharma was trading below its 2020 IPO valuation despite significant growth in the period since.

Like all investments, Royalty Pharma has risks. Attractive industries encourage competition and Blackstone LifeSciences has become a prominent competitor.15

If a medicine’s development fails, regulators reject or delay approval, or future safety issues emerge, the associated royalty stream might be worth little or nothing. Royalty portfolios sometimes rely on a small number of high-selling medicines, and royalties are time-limited as deals end and patents expire.

Nevertheless, we see Royalty Pharma as a diversified and lower-risk way to gain exposure to the long-term upside potential of medicine development and the biotech industry.

There are an estimated 6,000 to 10,000 rare diseases of which over 90 percent have no FDA-approved treatment.16 Several hundred new rare diseases are discovered or described each year.17 The opportunity is large; medicine is still in its infancy.

Chart 4: Royalty Pharma share price (US$)

Source: FactSet. Past performance is not indicative of future performance.

About the author

Alex Warnaar is an investment analyst at PM Capital. More PM Capital insights are available here.

Notes and references

1 Royalty Pharma, ‘Royalty Pharma plc Files 8-K Disclosing Positive Phase 3 Results for Daraxonrasib and Key Funding Developments, 14 April 2026, https://www.minichart.com.sg/2026/04/14/royalty-pharma-plc-8-k-filing-a….

2 Revolution Medicines, Daraxonrasib Demonstrates Unprecedented Overall Survival Benefit in Pivotal Phase 3 RASolute 302 Clinical Trial in Patients with Metastatic Pancreatic Cancer, 13 April 2026, https://ir.revmed.com/news-releases/news-release-details/daraxonrasib-d…

4 Barron’s, ‘This Biotech Stock Soars 39%. Pancreatic Cancer Trial was a Success’, 13 April 2026. https://www.barrons.com/articles/revolution-medicines-stock-pancreatic-…

5 Royalty Pharma, ‘Our Firm’, www.royaltypharma.com. Accessed 21 April 2026.

6 Royalty Pharma, ‘Royalty Pharma plc Files 8-K Disclosing Positive Phase 3 Results for Daraxonrasib and Key Funding Developments, 14 April 2026, https://www.minichart.com.sg/2026/04/14/royalty-pharma-plc-8-k-filing-a….

7 Royalty Pharma, Royalty Pharma Announces $3.3 billion Royalty Transaction with Cystic Fibrosis Foundation Therapeutics, 19 November, 2014.

8 Cystic Fibrosis Foundation, About Cystic Fibrosis, https://www.cff.org/intro-cf/about-cystic-fibrosis, Accessed 20 April 2026.

9 Royalty Pharma, Royalty Pharma Announces $3.3 billion Royalty Transaction with Cystic Fibrosis Foundation Therapeutics, 19 November, 2014.

10 Royalty Pharma, Royalty Pharma Reports Q4 and Full Year 2025 Results, 11 February 2026. https://www.royaltypharma.com/news/royalty-pharma-reports-q4-and-full-y…

11 Royalty Pharma, ‘Memorial Sloan Kettering Cancer Center: Enabling the Development of a New Research Factility,’ https://www.royaltypharma.com/responsibility/access-to-healthcare, Accessed 10 April 2026.

12 Royalty Pharma, Royalty Pharma Announces R&D Funding Collaboration for Chronic Immune-Mediated Diseases, 30 March 2026. https://www.royaltypharma.com/news/royalty-pharma-announces-rd-funding-…

13 Royalty Pharma, Investor Day transcript, September 11, 2025.

14 Royalty Pharma, Investor Day transcript, September 11, 2025.

15 Blackstone, ‘Teva and Blackstone Life Sciences Announce $400 Million Strategic Growth Capital Agreement to Advance duvakitug’, https://www.blackstone.com/news/press/teva-and-blackstone-life-sciences…, Accessed 4 May 2024.

16 US Government Accountability Office, ‘Rare Disease Drugs,’ https://www.gao.gov/products/gao-25-106774, Accessed 4 May 2026.

17 Pharma Research, ‘New Report: 800 New Medicines in Development to Treat Rear Diseases, https://phrma.org/blog/new-report-nearly-800-new-medicines-in-developme…, Accessed 4 May 2026.

Disclaimer

This information is issued by PM Capital Pty Limited (ACN 637 448 072) (‘PM Capital’), a corporate authorised representative of Regal Partners (RE) Limited (ACN 083 644 731, AFSL 230222) (‘Regal Partners RE’). Regal Partners RE is the Responsible Entity and issuer of PM Capital Global Companies Fund (ARSN 092 434 618) and has authorised the release of this information. PM Capital and Regal Partners RE are wholly owned subsidiaries of Regal Partners Limited (ACN 129 188 450, ASX:RPL) (‘RPL’) (RPL and its subsidiaries are referred to together as ‘Regal Partners’).

This information is subject to copyright and any use or copying of the information in it is unauthorised and strictly prohibited. All figures are in USD, unless stated otherwise.

Past performance is not indicative of future performance. All investments contain risk and may lose value. The objective and past returns of PM Capital Global Companies Fund (ARSN 092 434 618) are expressed after the deduction of fees and before taxation. The objective is not intended to be a forecast and is only an indication of what the investment strategy aims to achieve over the medium to long term. While we aim to achieve the objective, the objective and returns may not be achieved and are not guaranteed. Certain statements in this information may constitute forward looking statements. Such forward looking statements involve known and unknown risks, uncertainties, assumptions and other important factors, many of which are beyond the control of Regal Partners, and which may cause actual results, performance or achievements to differ materially (and adversely) from those expressed or implied by such statements.

This information has been prepared for general information purposes only and without taking into account any recipient’s investment objectives, financial situation or particular circumstances (including financial and taxation position). The information does not (and does not intend to) contain a recommendation or statement of opinion intended to be investment advice or to influence a decision to deal with any financial product, nor does it constitute an offer, invitation, solicitation or commitment by Regal Partners. You should consider the product disclosure statement (‘PDS’), prior to making any investment decisions. The PDS and target market determination (‘TMD’) can be obtained on this website. If you require financial advice that takes into account your personal objectives, financial situation or needs, you should consult your licensed or authorised financial adviser. This information is only as current as the date indicated, is subject to change without notice and may be superseded by subsequent market events or for other reasons. Regal Partners does not guarantee the performance of any fund or the return of an investor’s capital. None of Regal Partners or its related parties, employees or directors provide any warranty of accuracy or reliability in relation to this information and to the extent permitted by law, Regal Partners disclaims all liability (including liability for negligence) for direct or indirect loss or damage suffered by any recipient acting in reliance on this information.

Regal Partners RE, other members of Regal Partners or funds managed or advised by them may now, or in the future, have a position in any securities which are referred to in this information. Such positions are subject to change at any time without notice.