Annuities provider well positioned for rising interest rates and structural growth in retirement savings.

Key points

-

Higher interest rates will support demand for annuities, aiding Challenger’s earnings growth.

-

In the medium term, an ageing population, expected growth in retirement savings and regulatory reform should further underpin annuities demand.

-

Apollo Global Management Inc., a US private-equity and alternative-assets giant, has a minority 19.1% interest in Challenger. That provides opportunities for product innovation at Challenger and potential for corporate activity.

-

Challenger’s low price multiple1 provided an attractive entry point.1

Introduction

Established in 1985, Challenger is one of Australia’s largest active funds managers with $102 billion of group assets under management.2 The company is best known for Challenger Life, the dominant local provider of annuities with an estimated market share above 80%.3

Annuities are financial products offering lifetime or fixed-term payments. Investors in annuities choose if they want payments to last a fixed number of years, for their life expectancy, or for the rest of their life. Annuities typically suit retirees wanting more fixed income in their portfolio, lower risk and reliable income.

Challenger’s funds-management business comprises Fidante, a business that takes minority interests in separately branded funds-management firms. Challenger provides distribution, administration and business support to Fidante-affiliated firms, leaving managers of those firms to focus on managing investment portfolios. Fidante has a good mix of investment managers. Over three years, 80% of funds held through Fidante have outperformed their benchmark index.4

Shares in Challenger, (ASX: CGF), rallied from 2010 to 2017 (see Chart 1 below) as its funds under management grew more than threefold during that period.5 Challenger benefited from higher interest rates in the previous decade that supported annuities demand. The market liked Challenger’s dominant position in annuities, and its leverage to an ageing population and mandated growth in retirement savings.

Chart 1: Challenger share price

Source: Factset, PM Capital

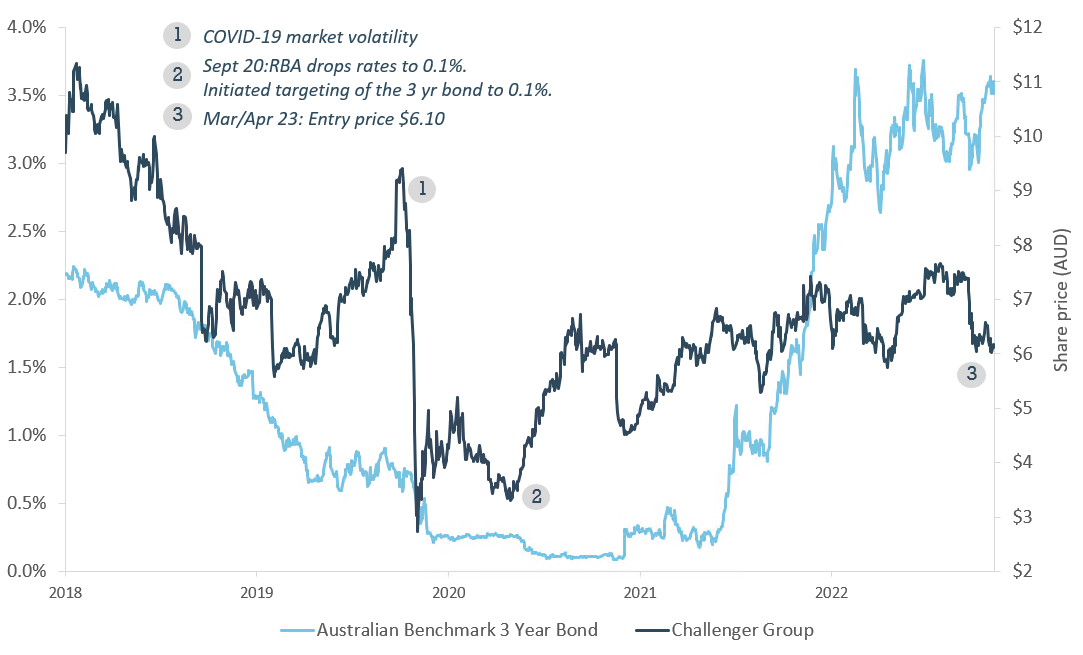

But after peaking near $14 in late 2017, Challenger fell below $4 in April 2020. That coincided with the Australian 10-year Bond yield falling from around 3% to below 1%. With interest rates near zero, annuities demand dried up.

Chart 2: Challenger share price since 2018

Source: Factset, PM Capital

Lower interest rates affect Challenger’s earnings. It profits from the difference between the investment returns it achieves from investing annuity contributions, and the annuity rates it is bound to pay investors. With interest rates in 2020 well below normal long-term levels, credit spreads (the excess corporate credit yield relative to the Government bond yield) contracted.

At the same time, volatile credit markets during COVID-19 led to the market questioning if Challenger had enough capital to withstand a credit crisis and global recession during the pandemic. As an APRA-regulated entity, Challenger must maintain sufficient capital to honour its obligations to its annuity investors. Spooked by credit concerns, the market sold shares in Challenger first and asked questions later.

Challenger had other problems. In 2020, it entered the banking market through acquiring MyLifeMyFinance Limited, an Australia-based customer and savings loan bank, for $35 million. The acquisition proved a distraction: the bank lacked the scale and capital requirements to expand. In October 2022, Challenger announced it would sell the bank to Heartland Group Holdings, a New Zealand company.

These and other problems culminated in a market perception that Challenger had lost focus and had a lacklustre outlook. The market was accustomed to strong growth in Challenger’s funds under management, but it had net fund outflows in the first half of FY23. The unexpected resignation of Challenger CEO Richard Howes in August 2021 added to the uncertainty. The market viewed Challenger as “ex-growth”.

However, PM Capital believed the market overreacted to Challenger’s problems and that it was oversold by first-quarter 2023. We built a position in Challenger in March and April 2023 an at average price of $6.10. Challenger is held in the PM Capital Australian Companies Fund.

These four factors support our positive view on Challenger:

1. Higher interest rates

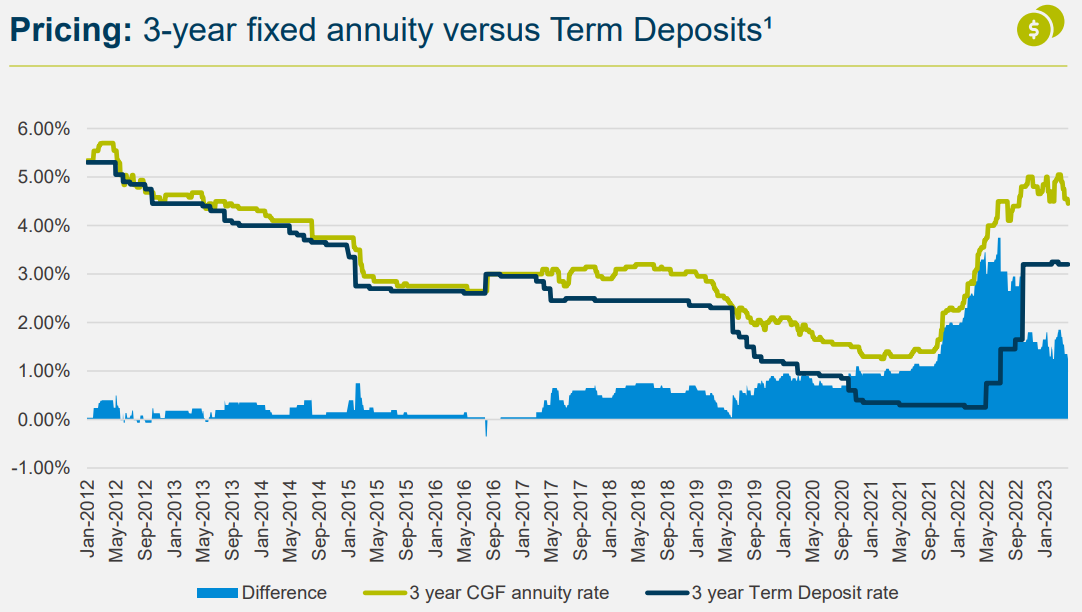

In its latest Investor Day presentation6, Challenger said the normalisation of Australian interest rates had made guaranteed-income products, such as annuities, more attractive. Challenger described it as the “best customer proposition (for annuities) in the last 10 years”. Current annuity rates are at their highest in a decade.

Chart 3 below compares Challenger’s three-year fixed annuity rate to bank term deposits. Note the sharp rise in the annuity rate (the green line on the chart) since 2021 and also the gap between returns from annuities and bank term deposits (the blue line). Challenger’s three-year annuity rate of 5.05% in March 20237 compares favourably to term deposits.

Chart 3: Challenger annuity rate (3-year fixed)

Source: Challenger Investor Day presentation, May 2023. RBA – comparison to end of April 2023. 1 Term deposits, where available, are averages of the five largest banks’ rates.

With annuity rates rising, demand for annuities from individual investors and financial advisers is increasing. Challenger said its quotation on annuities for advisers in the first half of FY23 was up 100% on the previous corresponding period.8 After shunning annuities when interest rates were near zero, more advisers are using them again.

At the same time, Challenger is focusing on longer-term annuities (2+ years) in new sales by “remixing” its annuity book. This should aid Challenger’s margins and maturity outlook on annuities, and also its competitive position with banks that compete mostly for short-duration deposits (1 year).

As high inflation persists this year, and with interest rates expected to rise further, conditions for annuity sales should continue to strengthen. We believe more retirees will seek investment products, such as annuities, that provide higher, reliable income (as living costs rise) and address market volatility.

2. Structural growth

Australia’s ageing population provides short- and long-term tailwinds for Challenger.

In the short term, demographers expect the number of “baby boomers” (born circa 1946-1964) entering retirement age (65+) to peak in the middle of this decade.9 That should mean a larger cohort of retirees seeking more defensive income-focused investment products in the next few years. Challenger argues that annuities can comprise 20-25% of a retiree’s portfolio (for income).10

Longer term, the number of people aged 65 and over in Australia is forecast to double to 8.9 million by 2060-61.11 By then, 23% of the population is projected to be 65 and older, from 16% in 2019-20. About 1.9 million Australians will be 85 or older by 2060-61.12

Moreover, as Australians live longer they are likely to seek annuities and other investment products that address longevity risk through guaranteed pensions. Australian life expectancy is among the highest globally and the average time in retirement is 24 years.13

Regulatory reform should also support annuities demand. The Retirement Income Covenant (RIC) requires super trustees to develop and document a retirement-income strategy for members. Effectively, the RIC means super funds will need to use more guaranteed income-style products (including annuities) in their portfolios. Parliament passed the RIC in February 2022 and it came into effect that July.

The Federal Government’s Quality of Advice Review (published in February 2023) and its work this year to legislate the objective of superannuation are also expected to encourage greater focus on income investing in retirement. That’s good for annuities.

3. Apollo Global Management/innovation

In December 2022, Apollo increased its holding in Challenger to 19.1%, prompting speculation that the latter is a takeover target. There has also been speculation in the past few years that other private equity firms could acquire Challenger.

Apollo Global Management comprises Apollo Asset Management (the alternative-assets business) and Athene, its retirement-services business (the two businesses merged in January 2022). In July 2021, Athene said it and Challenger “share the same mission” to provide retirement security and described Challenger as a “perfect partner” for it.14

Although an eventual takeover of Challenger by Apollo is possible, the short-term focus is on building a strategic partnership. In February 2022, Challenger and Apollo announced a Joint Venture (equally owned) to bring innovative new non-bank lending solutions to Australia and New Zealand through a direct lending platform.

PM Capital expects Challenger to harness Apollo’s extensive product innovation and asset management capabilities. Capitalised at US$46 billion on the New York Stock Exchange15, Apollo (NYSE: APO) is a global leader in its field. Challenger needs to be more innovative to address market concerns that it has a sluggish growth outlook.

Challenger’s JV with Apollo is part of a broader transformation. In recent years, Challenger has done much to simplify the business and diversify its revenue. The sale of Challenger Bank (expected to close in the first half of FY24) will help refocus Challenger, return $90 million of excess capital (in two tranches),16 and strengthen its capitalisation.

Recent contract wins at Artega Investment Administration (born out of Challenger and Fidante) are another good sign, as are Challenger’s strategic partnerships in real estate with Elanor Investors Group (Challenger is expected to own 13.7% of Elanor after announcing in June 2023 the sale of its real estate funds management to Elanor); MS&AD Insurance Group Holdings (for Japanese distribution of Challenger’s annuities) and with Apollo. Much work needs to be done, but Challenger is accelerating its strategy to diversify revenue.

4. Valuation

When PM Capital initiated a position in Challenger at $6.10 in early 2023, it traded on a Price Earnings (P/E) multiple of about 12 times. We believe this valuation is undemanding given the company’s dominant position in annuities, its leverage to rising rates and growth in retirement savings, and its partnership with Apollo.

Several years of low interest rates depressed Challenger’s earnings. PM Capital believes Challenger should trade on a normalised PE of around 15 times.

As Challenger’s earnings growth increases over the next few years, we expect the market to ascribe a higher valuation multiple to it. This combination of stronger earnings growth and a larger PE multiple can drive a sustained re-rating of a stock.

Conclusion

Although PM Capital has a positive view on Challenger, we do not expect it to deliver the same rate of growth it provided for much of the previous decade as annuities are a competitive market. However, we believe Challenger has a strong market position and excellent brand recognition.

A reduction in financial advisers is another issue for Challenger, whose largest product distribution channel is through financial intermediaries. The number of financial advisers in Australia fell 17% in 2022, the lowest in almost two decades.17 A higher compliance burden for financial advisers, following the Financial Services Royal Commission, has encouraged more advisers to leave the industry. Annuities sold to retail investors through financial advisers provide higher margins for Challenger compared to annuities written for institutional clients.

Challenger has also had much recent change (it appointed Nick Hamilton as CEO in January 2022, an internal appointment). The business is being reorganised, improving its customer focus, building its presence with direct investors, and increasing product innovation. That creates opportunity but also implementation risk.

In spite of these challenges, PM Capital believes Challenger’s valuation has not adjusted sufficiently to recognise its improving prospects as interest rates rise.

About the author

John Whelan is co-Portfolio Manager of the PM Capital Global Companies Fund and PM Capital Australian Companies Fund. More PM Capital stock and market insights are available here.

Notes:

1$6.19 at 16 June 2023.

2Challenger. “Third Quarter AUM Annuit Sales and Net Flows”. 20 April 2023

3Current industry estimates of Challenger’s share in the Australian annuities market range from 80-90%. Challenger reported 75% market share in annuities in 2020.

4Challenger Investor Day Presentation. May 2023. P43

5Challenger’s total assets under management of $81 billion in first-quarter FY19 compared to $25.5 billion in first-quarter FY11.

6Challenger Investor Day Presentation. May 2023

7ibid

8Challenger Investor Day Presentation. May 2023

9Salt, Bernard. “Turning Point: the 2020s baby boom retirement surge”. FirstLinks 24 March 2021.

10Challenger Investor Day Presentation. May 2023

11Federal Government, “2021 Intergenerational Report: Australia over the next 40 years”. June 2021. The doubling occurs from 2019-20 levels.

12ibid

13Challenger Investor Day Presentation. May 2023. P6

14Athene Holding, “Athene leads minority investment in Australia’s Challenger Ltd. 6 July 2021.

15At 15 June 2023

16Challenger Investor Day Presentation. May 2023. $50 million of excess capital has already been returned. Another $40 million will be returned prior to completion of the sale.

17Williamson, J. “Adviser Population Dropped 17% in 2022.” Financial Standard 13 January 2023.

This insight is issued by PM Capital Limited ABN 69 083 644 731 AFSL 230222 as responsible entity for the PM Capital Australian Companies Fund (ARSN 092 434 467), the "Fund". It contains summary information only to provide an insight into how we make our investment decisions. This information does not constitute advice or a recommendation, and is subject to change without notice. It does not take into account the objectives, financial situation or needs of any investor which should be considered before investing. Investors should consider the Target Market Determinations and the current Product Disclosure Statement (which are available from us), and obtain their own financial advice, prior to making an investment. The PDS explains how the Fund's Net Asset Value are calculated. Past performance is not a reliable guide to future performance and the capital and income of any investment may go down as well as up.