Inside the Enhanced Yield Fund (EYF):

Essential Infrastructure – Road to recovery.

Introduction

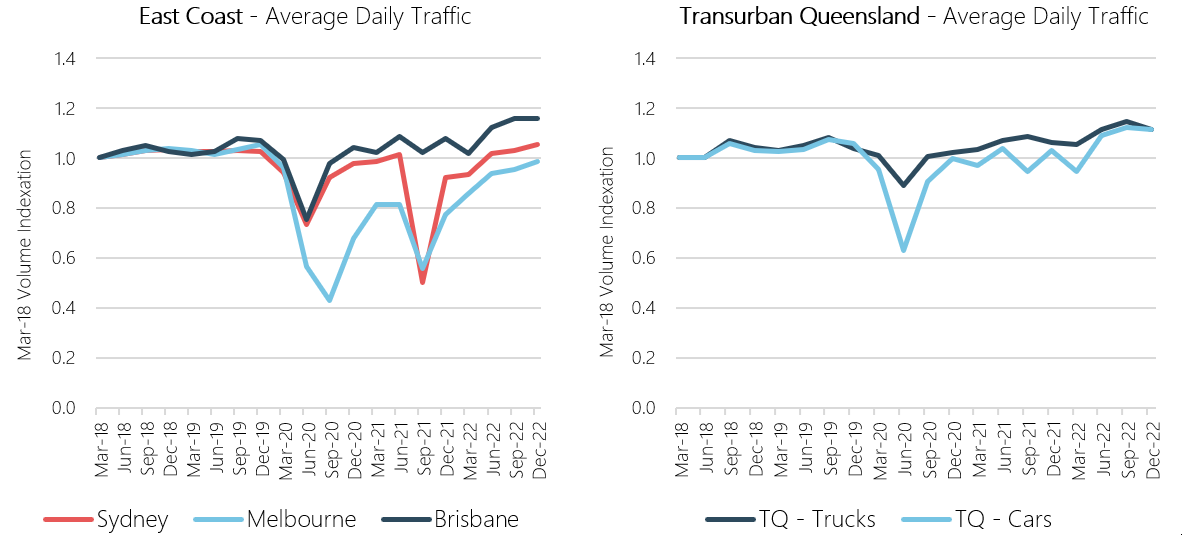

During the COVID-19 pandemic, the number of cars using toll-roads for their daily commutes fell materially as – among other things - more people began to work from home. In response to this, the yield premiums above cash that markets started to pay for investing in the bonds of toll-road companies increased notably. This caught our eye.

Essential infrastructure assets are among the highest quality assets which one can invest in. However, equally important is the business model that has been positioned around each asset – such as the amount of debt held against it, the ability to increase tolls over time, etc.

Transurban Queensland and ConnectEast are two such examples of high-quality toll-road operators in our backyard.

Transurban Queensland operates a monopoly network of corridor roads across Brisbane. It effectively controls what is known as the Brisbane toll-road “orbital” – essentially the entire toll-road network in Brisbane. Capitalising on a high proportion of truck traffic (forming as much as 50% of revenues in Queensland), we analysed the earnings strength of these unique assets.

ConnectEast exhibits similar jewel asset features. Owning core traffic corridors into the Melbourne CBD and across the Mornington Peninsula, it maintains a considerable travel time advantage over the circa 45 traffic light junctions sprawled across the free road options to their toll-road.

1. What happened with traffic?

Contrary to popular belief, the rebound in traffic happened very quickly. After analysing numerous essential infrastructure models, i.e. airplanes, buses, rail and ride-share, we noticed a clear trend – i.e. that car and truck traffic were showing signs of being the most resilient during the COVID-19 downturn.

Further, cash flows and margins held up nicely – all while we continued to witness the rapid return of traffic to beyond 2019 levels.

These were precisely the features of businesses that we like to own i.e. where pricing moves with markets, but the underlying assets are good quality and have steady cash flows.

2. The durability of the truck revenue model

With highly residential streets in the lead-in to major cities and a major Australian trade network, there is limited room to transport freight and fast-moving consumer goods via rail. Indeed, truck is the only option for many across the supply chain.

Further, sustaining >95% of 2019 truck traffic throughout the most severe lockdown scenarios was a remarkable result. Trucks additionally produce a 3x revenue multiplier on various roads, providing a consistent buffer and contributing ~40-60% to revenue growth.

As (A) freight growth continues and (B) congestion remains a key issue, trucks are increasingly being diverted to the toll-road corridors – enabling greater revenues for operators hand-in-hand with cleaner, quieter residential streets.

Source: Transurban, PM Capital

3. Pricing and operating margin tailwinds

With pricing of tolls able to be increased as inflation climbs – it builds protection into the long term cashflows produced by these assets. Further, with these price increases front-loaded, the pricing benefits deliver compounding returns over the course of the investment.

In terms of operating earnings, there has been strong cost containment, delivering impressive operating margins coming into 2023. These feed directly into stable liquidity and more than offset any increases in debt costs that the businesses may have faced. As an additional credit support, these operators have hedged out rate risk in their borrowing portfolios.

Overall, we see both inflation and interest rates risk well mitigated by the nature of the business model and proactivity of management.

Conclusion

As traffic volumes continue to grow, we remain well positioned with our investments.

Having focussed on the performance of the underlying assets, and not market hysteria, we quickly spotted the ability for these unique assets to weather the darkest parts of the storm, allowing us to invest in essential Australian infrastructure assets at attractive yields.

In late 2022, having invested in ConnectEast’s 3Y senior bonds at a ~5.5% yield and Transurban Queensland’s 2023 senior bonds at ~4.5%, we locked in yields well in excess of the RBA cash rate for two strongly cash generative businesses - a welcome addition to the Fund.

This is a great example of the sort of investments we look to add to the Enhanced Yield Fund, highly cashflow generative monopoly assets, that are out of favour with the market for the wrong reasons.

This insight is issued by PM Capital Limited ABN 69 083 644 731 AFSL 230222 as responsible entity for the PM Capital Enhanced Yield Fund (ARSN 099 581 558, the ‘Fund’). It contains summary information only to provide an insight into how we make our investment decisions. This information does not constitute advice or a recommendation, and is subject to change without notice. It does not take into account the objectives, financial situation or needs of any investor which should be considered before investing. Investors should consider the Target Market Determinations and the current Product Disclosure Statement (which are available from us), and obtain their own financial advice, prior to making an investment. The PDS explains how the Fund’s Net Asset Value is calculated. Past performance is not a reliable guide to future performance and the capital and income of any investment may go down as well as up.