Nevada Gold Mines – A turning point in the high desert?

By Andrew Russell

Forget the bright lights of the Vegas Strip. I recently returned from a much dustier, much more lucrative corner of the Silver State: the Nevada Gold Mines (NGM) complex owned and operated by Barrick in a joint venture with Newmont; a portfolio holding and our largest gold exposure. If you follow the mining sector, you know this isn't just any ‘site’. It is the largest gold mining complex on the planet – a sprawling ‘constellation of assets’ that includes 12 open pits, 10 underground mines, and a metallurgical puzzle that would make a chemistry professor weep.

The goal of this visit was simple: to determine if this massive joint venture between Newmont and Barrick is finally turning a corner or if the ‘industrial logic’ that birthed it in 2019 is being swallowed by the Nevada desert.

The 2019 ‘Marriage of Convenience’ vs. Reality

In 2019, Barrick and Newmont did the unthinkable: they tore down the ‘fences’ between their adjacent properties in the Carlin and Cortez trends. The ‘industrial logic’ was to save $500 million a year by simply sending ore to the closest processing facility rather than the one owned by the ‘right’ company.

However, between 2H19 and early 2026, the operational trajectory diverged significantly from those early, rosy projections.

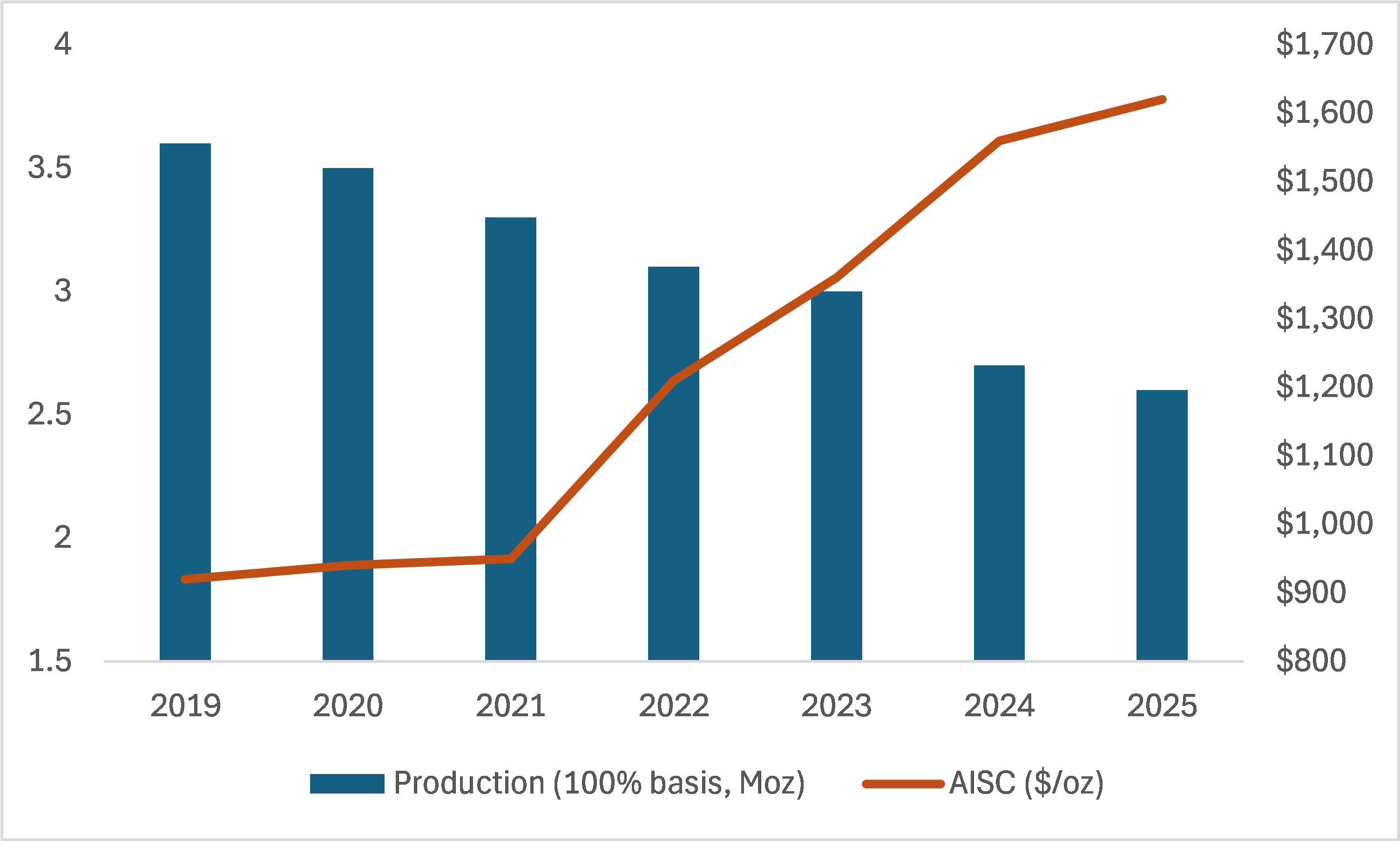

PRODUCTION vs AISC – PRODUCTION DECLINING – COSTS INCREASING

Source: Barrick annual reports

The rise in All-In Sustaining Costs (AISC) from sub-$1,000 to over $1,600 per ounce was driven by a brutal cocktail of lower-than-expected grades, sector-wide inflation, and a massive bill for deferred maintenance.

"Collapsing Structures" and the Great Fix

The most visceral part of the tour was seeing the state of the inherited infrastructure. By 2024, the internal dialogue at NGM had turned grim, with analyst briefings referencing ‘collapsing structures’, corroding Carbon-in-Leach (CIL) tanks, and leaking cyanide vessels. It turns out the synergies captured in the early years were partly a result of delaying required maintenance from the pre-JV era.

The 2021 mechanical failure of the Goldstrike Roaster was the wake-up call. This facility is critical for processing double refractory ore — rock containing both sulphides and organic carbon that effectively robs gold from cyanide solution if not oxidized at high temperatures. When it failed, production plummeted and costs spiked as the mine was forced to feed lower-grade stockpiles just to keep the lights on.

However, the good news is that the rectification strategy deployed by Barrick – the JV's operator – is gaining genuine traction. Here is the 2026 scoreboard for the major fixes:

- Sage Autoclave (Turquoise Ridge): Historically capped at 80% availability due to wear. Following a total overhaul, it is targeting 95% availability, which should inevitably drag processing costs back down.

- Gold Quarry Roaster (Carlin): Throughput is up 16% following a multi-stage expansion. Importantly, unit costs are trending toward lower.

- CIL Tank Farms: The structural corrosion that once threatened containment has been addressed with emergency steel replacement and relining, restoring the recovery rates that had been slipping.

In short: the plant reinvestments are finally starting to pay off.

The Geological Headache

Mining in Nevada isn't just about digging; it's about chemistry. NGM deals with incredibly complex ore blending. If your geological model underestimates the carbon content, your recovery rates in the autoclave plummet. If you overestimate the grade, the fixed costs of underground mining destroy your margins.

For years, grade reconciliation – the difference between what the models predicted and what the mill produced – was a major source of friction, especially at Cortez and Carlin.

The Good News: The geologists I met on-site confirmed that reconciliation is back within the targeted +/- 5% margin of error. This was achieved through a massive increase in the drilling program and a high-tech pivot to AI-driven exploration – using machine learning to analyse massive geochemical and satellite datasets to find deep-seated deposits that traditional drilling might miss.

The Human Element: Autonomous Trucks vs. The “Great Resignation”

One of the most sobering stats from the tour: historically, 58% of employees leave within three years. They get trained, and then they get poached by competitors. It’s not really a wages issue – dump truck drivers are making US$45-48/hr – it’s simply difficult to find people willing to work in the high desert, especially for underground roles and younger workers.

To fight this, NGM has gone "all-in" on technology and re-worked the incentive structure:

- Autonomous Trucking: This has been a gamechanger, leading to a 20% increase in efficiency. The trucks run smoother, stop less, and carry full loads with less wear and tear. Expect this to also lead to an easing in labour constraints.

- Retention bonuses: Starting in January 2026, monthly bonuses were introduced and linked directly to delivery targets to boost retention.

While turnover spiked significantly during the covid period, this is now back to where it was pre-covid (12-14%) with the aim to get below 10%.

The Elephant in the Room: The Newmont-Barrick Brawl

While the operations are stabilizing, the boardroom is a different story. In February 2026, Newmont announced that they had issued a ‘Notice of Default’ to Barrick. The accusation? That Barrick has been diverting JV resources – including specialized equipment and technical experts – to speed up development at Fourmile.

The Fourmile Drama:

- The Asset: Fourmile is a high-grade ‘jewel’ that sits right next to the JV’s Goldrush mine and identified as one of the century’s most significant gold discoveries.

- The Dispute: Fourmile is owned 100% by Barrick, not the JV. Newmont is understandably frustrated that the ‘declining value’ of the JV is being offset by a project they don't own.

- The ‘NewCo’ Gambit: Barrick wants to spin off its North American assets into a new public entity via IPO in 2026. Newmont is likely using this performance critique as leverage to get a better deal.

Conclusion: Is the Rectification Real?

While Barrick offers greater exposure to Nevada, we don’t see the need to pay a higher multiple for the Barrick portfolio that carries significantly more jurisdictional risk in Africa. We maintain our preference for Newmont, which we view as offering a more attractive free cash flow yield which should flow back to investors in the form of increased dividends and buybacks, and a higher-quality broader portfolio at a cheaper entry point.

NGM remains in our opinion the premier gold complex on the planet. The problems have been understood, the remedies are in place, and the performance is finally following suit. The ‘rectification’ is real – the only question is whether the parents can stop fighting long enough to let us collect the dividends.

Disclaimer

This information is issued by PM Capital Pty Limited (ACN 637 448 072) (‘PM Capital’), a corporate authorised representative of Regal Partners (RE) Limited (ACN 083 644 731, AFSL 230222) (‘Regal Partners RE’). Regal Partners RE is the Responsible Entity and issuer of PM Capital Global Companies Fund (ARSN 092 434 618) and has authorised the release of this information. PM Capital and Regal Partners RE are wholly owned subsidiaries of Regal Partners Limited (ACN 129 188 450, ASX:RPL) (‘RPL’) (RPL and its subsidiaries are referred to together as ‘Regal Partners’).

This information is subject to copyright and any use or copying of the information in it is unauthorised and strictly prohibited. All figures are in USD, unless stated otherwise.

Past performance is not indicative of future performance. All investments contain risk and may lose value. The objective and past returns of PM Capital Global Companies Fund (ARSN 092 434 618) are expressed after the deduction of fees and before taxation. The objective is not intended to be a forecast and is only an indication of what the investment strategy aims to achieve over the medium to long term. While we aim to achieve the objective, the objective and returns may not be achieved and are not guaranteed. Certain statements in this information may constitute forward looking statements. Such forward looking statements involve known and unknown risks, uncertainties, assumptions and other important factors, many of which are beyond the control of Regal Partners, and which may cause actual results, performance or achievements to differ materially (and adversely) from those expressed or implied by such statements.

This information has been prepared for general information purposes only and without taking into account any recipient’s investment objectives, financial situation or particular circumstances (including financial and taxation position). The information does not (and does not intend to) contain a recommendation or statement of opinion intended to be investment advice or to influence a decision to deal with any financial product, nor does it constitute an offer, invitation, solicitation or commitment by Regal Partners. You should consider the product disclosure statement (‘PDS’), prior to making any investment decisions. The PDS and target market determination (‘TMD’) can be obtained on this website. If you require financial advice that takes into account your personal objectives, financial situation or needs, you should consult your licensed or authorised financial adviser. This information is only as current as the date indicated, is subject to change without notice and may be superseded by subsequent market events or for other reasons. Regal Partners does not guarantee the performance of any fund or the return of an investor’s capital. None of Regal Partners or its related parties, employees or directors provide any warranty of accuracy or reliability in relation to this information and to the extent permitted by law, Regal Partners disclaims all liability (including liability for negligence) for direct or indirect loss or damage suffered by any recipient acting in reliance on this information.

Regal Partners RE, other members of Regal Partners or funds managed or advised by them may now, or in the future, have a position in any securities which are referred to in this information. Such positions are subject to change at any time without notice.