Although we are a long term investor, there are some trends to be found in the latest Australian earnings season, says Uday Cheruvu.

My key takeaway is that the main attraction for investors now is growth potential. Most of the growth stocks in the Australian market, such as Afterpay, WiseTech Global and Altium, or even the likes of Domino's, have reported average to good results. The market has received them well and bid the stock up to all-time highs, however, so investors are certainly paying up for their access to these stocks. More generally, the Australian market is trading at 20 times forward earnings – a significant valuation - but investors seem sanguine about the risks involved.

This is a time to look back and assess what is giving real value and long term growth potential. At this time therefore you need to be patient and wait for the right opportunities to show themselves.

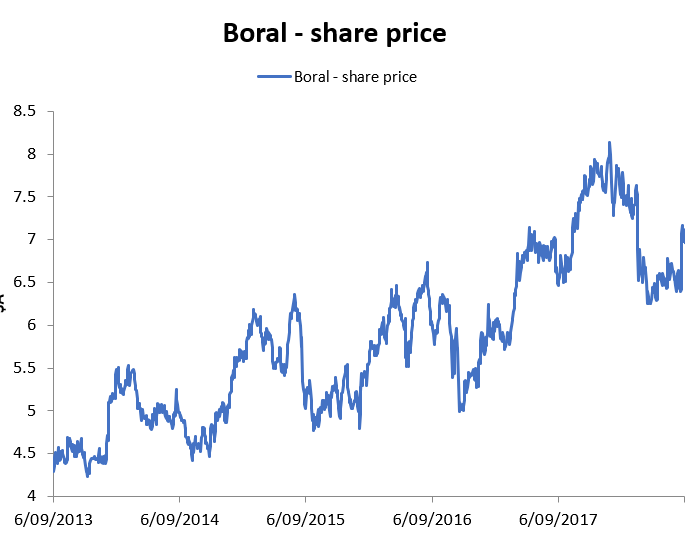

One of the interesting areas is those stocks with offshore exposures. A year ago we were concentrating on companies with offshore earnings. This was based on our view that global growth was going to be stronger than Australian growth. We still hold that view but we are cognisant of the fact that some Australian companies are now going off shore in an attempt to chase growth. That is likely to be a dangerous track to take. We believe that companies such as Boral have shown what buying a good business overseas can achieve. So therefore we think that the trend of companies with off shore earnings doing well will continue.

Boral’s good results were bolstered by its 2016 acquisition of the US fly ash, roofing, stone and light building company Headwaters for $US2.6 billion. There were some doubts if Boral could safely and effectively fold the company into its current US operations. However, the result dissipates some of the uncertainty. Some investors will still continue to doubt but the fact that the $US100 million synergy targets that they forecast have increased, and the fact that they're looking at high 10-20% growth in the US next year gives a perspective that there is a lot of potential in the US business.

When we look at where we like to see geographic expansion, it doesn't matter whether it is in the US, China, or Europe, as long as they understand those markets and know how to actually operate in them. That's when we think the company benefits. So therefore when we look at companies like Boral that has been in the US market for a long time we think that they will do well.

While not an earnings announcement, the announced merger between TPG and Vodafone during the earnings period has interesting ramification for the sector. We think Telstra will be the biggest beneficiary from this corporate action as currently its earnings are coming under pressure, particularly its profitability in the mobile business. TPG’s aggressive pricing in mobile has forced the pricing down for the rest of the sector.

With the merger of TPG and Vodafone, we think there's potential that pricing will come back, i.e. the pricing will start going up because Vodafone's culture has been more towards customer service and quite a premium pricing. TPG grew its business by cutting costs. While our view is that this merger is a positive move, it will take a long time to bed in and there will be some teething issues. We will be looking at the opportunities in the sector to see when value shows itself.