Investor in copper and rail assets trading at signficant discount to the value of its underlying holdings.

By Kevin Bertoli, PM Capital

Key points

- Grupo Mexico holds majority stakes in Southern Copper Corp and GMexico Transportes, a freight rail operator.

- Through Southern Copper, Grupo Mexico is leveraged to favourable dynamics in copper, a commodity PM Capital favours due to ongoing supply constraints and rising demand from renewables.

- GMexico Transportes has steadily grown its earnings over the past five years and is well-positioned to benefit from ‘reshoring’ as more offshore manufacturing returns to the US.

- Grupo Mexico trades at a steep discount to the value of its holdings in Southern Copper and GMexico Transportes – and provides a cheaper entry point to Southern Copper’s earnings and dividend streams.

Introduction

Listed on the Mexican Stock Exchange (BMV), Grupo Mexico SAB de CV (BMV: GMEXICOB) is one of Mexico’s largest companies, capitalised at 692.3 billion Mexican pesos1.

The Mexican conglomerate has two key assets that account for most of its valuation: an 89.9% stake in Southern Copper, a US-listed copper producer; (NYSE: SCCO); and a 70% stake in GMexico Transportes, Mexico’s largest rail freight operator (BMV: GMXT).

Copper is the main driver of Grupo Mexico’s earnings, accounting for about 80% of its revenue and 90% of its Earnings Before Interest and Tax (EBIT) in 2022. The transport/rail division mostly accounts for the rest of Grupo Mexico’s revenue and earnings.

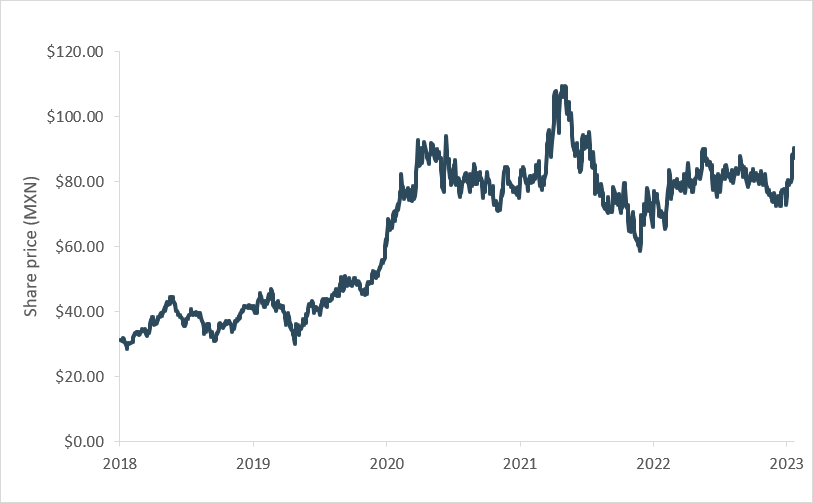

PM Capital initiated a position in Grupo Mexico in July 2023 at around MXN$82 a share. We added to that position in October and November 2023 during volatility in Grupo Mexico’s share price. At the time, copper-price weakness (due to market expectations of a copper surplus in 2024 and fears of global recession) weighed on investor sentiment towards Grupo Mexico.

Chart 1: Grupo Mexico share price

Source: Bloomberg

Grupo Mexico traded at a large discount to the market value of its investments in Southern Copper and GMexico Transportes. That was partly due to Grupo Mexico’s conglomerate structure - multi-division firms often attract a lower multiple to their earnings and cash flow - and also because Mexico is an emerging economy perceived to have higher regulatory risk.

We believed the market misunderstood the true value of Grupo Mexico’s assets and its improving long-term prospects. Short-term negative sentiment due to macro-economic fears created an opportunity for us to buy Grupo Mexico at a bottom-quartile valuation.

The following three factors underpin our positive view on Grupo Mexico:

1. Copper exposure

Copper is a key theme for PM Capital and the source of several successful holdings in our Global Companies Fund and Australian Companies Fund in the past few years.

In late 2019 and 2020, we initiated positions in leading copper companies, believing the copper price would rise due to underinvestment in new supply of the metal and ongoing supply disruptions.

On the demand side, growth in renewables would support the copper price. Copper is an essential material in Electric Vehicles and renewable-energy systems. Previous PM Capital insights explain our view on copper in more detail.

We maintain a positive long-term view on copper. Recent developments in key copper producers further confirm our copper thesis because they suggest ongoing supply challenges for the metal (see ‘Copper supply: recent developments'').

In addition, PM Capital was familiar with Southern Copper, having owned it previously. Capitalised at US$64 billion2, Southern Copper operates mines in Mexico and Peru. The company produces about 1 million tonnes per annum and sits in the bottom-quartile of the production cost curve, meaning it is among the world’s lowest-cost copper producers.

Through its stake in Southern Copper, Grupo Mexico is the largest copper producer in Mexico and Peru; the fourth-largest copper producer worldwide; provides exposure to the largest copper reserves in the world; and has the lowest extraction costs in the global copper industry (reflected in bottom-quartile production cost).3

2. Rail operations

Through GMexico Transportes, Grupo Mexico has a leading position in Mexico’s freight rail market. The duopolistic market comprises GMexico Transportes and Canadian Pacific Kansas City, a Toronto-listed rail operator (TSE: CP).

Unlike US freight rail companies that own the majority of US railroad tracks, Mexico’s two main rail operators operate under long-term government concessions. GMexico Transportes’ key concession runs until mid-2050, with exclusivity until the mid-to-late 2030s.

In late 2023, Grupo Mexico’s valuation discount to its underlying holdings in GMexico Transportes and Southern Copper widened amid fears the rail business would have to forfeit some of its assets to the Mexican government.

Mexico is in the process of building a rail alternative to the Panama Canal, known as the Interoceanic Corridor of the Isthmus of Tehuantepec. CITT will link the ports of Salina Crux on Mexico’s west coast with Coatzacoalcos, a port city on its east coast. As part of the project, the government repatriated 127 kilometres of GMexico Transportes’ 11,000-plus kilometres rail network.

Shares in GMexico Transportes’ fell on the news, but have since recovered most of their losses.4 The Mexican government and GMexico Transportes’ later agreed the rail operator’s remaining concessions would be extended for eight years (as compensation) for returning the 127-kilometre line to the government.

The news reinforced the additional regulatory risks that companies in emerging economies can face. But it also highlighted the market’s propensity to over-react to news and create opportunity for value-focused, long-term investors.

In December 2023, GMexico Transportes’ valuation discount to its holdings in Grupo Mexico Transportes and Southern Copper was the highest in at least five years. That’s despite the rail business accounting for only around 10% of Grupo Mexico’s earnings.

Over the past five years, the rail business has delivered compound annual growth of around 2% in freight volume and 4% in pricing. In our view, GMexico Transportes’ can continue to provide a stable, growing earnings stream over the long term.

The global trend towards near-shoring and reshoring – where offshore companies move more of their supply chain back to their home country due to heightened global risks - favours GMexico Transportes’.

In September, Canadian National and Union Pacific, two key Northern American rail operators, partnered with GMexico Transportes’ to create an intermodal service between points in Mexico, Canada and the US (through Chicago). Greater integration of Mexican rail freight into Northern American rail networks is positive for GMexico Transportes’.

3. Valuation

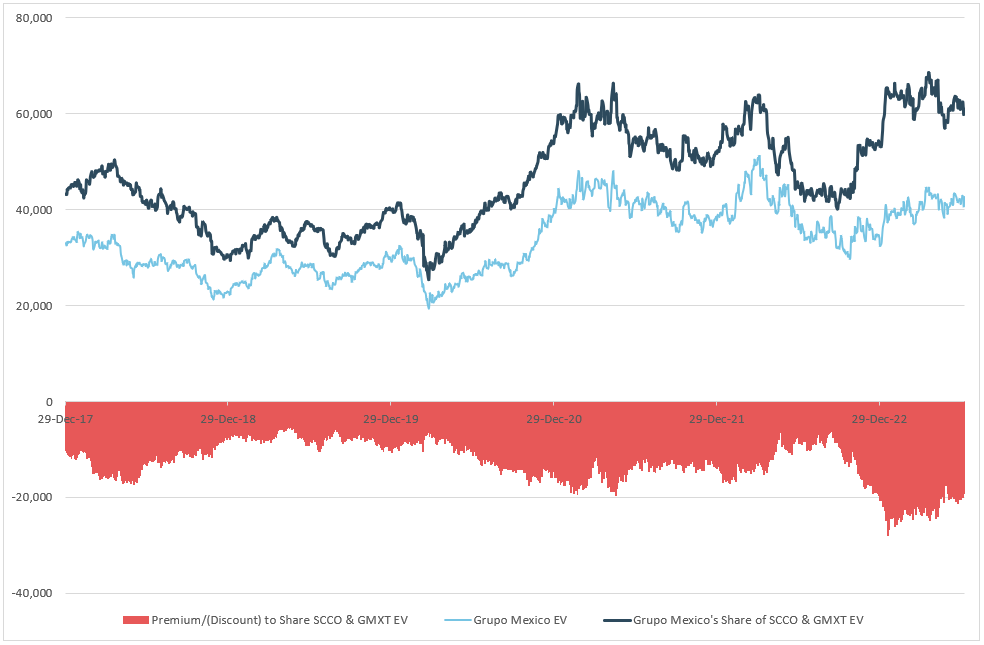

As mentioned, Grupo Mexico trades at a significant discount to the value of its underlying holdings in Southern Copper and GMexico Transportes.

Chart 2 below shows this discount over the past five years. The light blue line represents Grupo Mexico’s enterprise value (equity plus net debt). The dark blue line shows the combined enterprise value of Southern Copper and GMexico Transportes’. The red bars at the bottom of the chart track the valuation discount.

Chart 2: Grupo Mexico’s valuation discount

Source: PM Capital

Two things stand out. First, Grupo Mexico consistently trades at a discount to the value of its underlying assets. Second, the discount significantly widened in 2023 due to short-term market fears – a key reason PM Capital initiated a position in the stock.

A comparision with Southern Copper is also telling. At a US$4 copper price (per pound), Southern Copper trades at 17-18 times its FY24 earnings, our analysis shows. In contrast, Grupo Mexico trades at 10-11 times FY24 earnings, even though it owns 89.9% of Southern Copper.

Moreover, Southern Copper and GMexico Transportes pay out most of their free cash flow as dividends. In turn, Grupo Mexico returns that cash to its shareholders. At the US$4 copper price, Grupo Mexico yields about 5%.

Conclusion

Grupo Mexico is a good example of PM Capital’s investment processes to scour the world for companies that provide exposure to its favoured themes, in this case, copper.

Grupo Mexico also highlights our approach to identify assets trading at bottom-quartile valuations due to short-term volatility or irrational market pricing. Through Grupo Mexico, we have exposure to Southern Copper at a sharply lower valuation multiple (compared to investing in Southern Copper directly).

Finally, our view on copper emphasises PM Capital’s long-term approach. Our positive thesis on copper is based on multi-year commodity cycles. We view short-term weakness in the copper price as a potential opportunity to add exposure to a metal that has favourable prospects over this decade – a strategy reflected in our Grupo Mexico holding.

About the author

Kevin Bertoli is the co-Portfolio Manager of PM Capital’s Global Companies Fund and Australian Companies Fund. PM Capital is a leading asset manager in Australian and global equities, and interest rate securities. More PM Capital Insights are available here.

1 At 19 December 2023.

2 At 19 December 2023

3 Source: Grupo Mexico website. www.gmexico.com/en/Pages/divisions.aspx

4 Based on MXN$37 share price for Grupo Mexico Transportes at 19 December 2023.

This Insight is issued by PM Capital Limited ABN 69 083 644 731 AFSL 230222 as responsible entity for the PM Capital Global Companies Fund (ARSN 092 434 618), the "Fund". It contains summary information only to provide an insight into how we make our investment decisions. This information does not constitute advice or a recommendation, and is subject to change without notice. It does not take into account the objectives, financial situation or needs of any investor which should be considered before investing. Investors should consider the Target Market Determinations and the current Product Disclosure Statement (which are available from us), and obtain their own financial advice, prior to making an investment. The PDS explains how the Fund's Net Asset Value are calculated. Past performance is not a reliable guide to future performance and the capital and income of any investment may go down as well as up.